Understanding Contango and Backwardation In The Oil Futures Market

Retail investors can’t speculate on oil prices by taking physical delivery of a train car full of West Texas Intermediate (WTI) crude. The cost of delivery, storage and logistics make it wildly impractical.

Instead, investors can get exposure through futures contracts or through various exchange-traded funds (ETFs) that hold those contracts. But this isn’t as simple as clicking "buy" and holding.

The oil futures market, like other commodity futures markets, has its own characteristics, and two concepts are especially important to understand before diving in: contango and backwardation.

What is contango?

A futures curve plots the prices of contracts for delivery at different points in time. In the case of crude oil, this curve helps investors see how markets are pricing future delivery months ahead relative to today’s spot price.

Contango occurs when futures prices are higher than the current spot price. In this scenario, the futures curve slopes upward.

This structure reflects a wide range of factors that include storage costs, insurance and expectations of excess supply relative to demand.

For investors holding front-month oil futures (those closest to expiration) this matters because futures contracts must be rolled forward to the next month to maintain exposure.

As the futures contract nears maturity, its price converges toward the spot price. To remain invested, you have to sell the expiring futures contract and buy the next one.

In a contango market, the futures price will decrease relative to the spot price, even if both spot prices and futures prices are rising overall. This results in what’s known as negative roll yield, and it can erode returns over time, even if spot prices don’t move.

In the following chart of a hypothetical oil futures curve in contango, we assume a spot price of $70. Each subsequent futures contract increases in price, illustrating how, if this contango persisted, an investor rolling monthly would repeatedly pay more to stay invested.

This structural headwind is a big reason why contango poses a real cost to passive long holders in oil futures markets. However, contango doesn’t mean that overall returns will necessarily be negative. It just lowers potential returns.

What is backwardation?

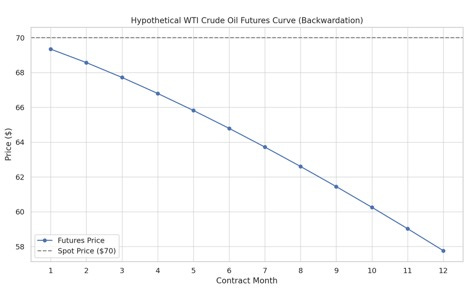

The opposite of contango is called backwardation. In a backwardated futures curve, the spot price is higher than the futures prices.

This setup can occur for a range of reasons including during periods of acute supply tightness, geopolitical disruption or when demand is unexpectedly strong and producers can’t quickly ramp up output.

When the curve is backwardated, futures contract prices will increase relative to the spot price as the expiration date approaches. This dynamic creates what’s known as positive roll yield, a tailwind for investors holding futures contracts.

In the chart below, you can see a hypothetical backwardated WTI crude oil futures curve starting at $70 spot and declining with each successive month.

A long investor who rolls monthly would effectively be pocketing the difference between the higher sale price and the lower purchase price, provided the curve remains in this state. Again, the gradual impact of roll yield applies throughout the holding period. It’s just that at the point of the roll is when the unrealized gain/loss becomes a realized one.

This is why backwardation is generally favorable for long-oriented oil ETFs and strategies. However, just as contango does not mean overall returns will be negative, backwardation does not guarantee a positive return.

IMPORTANT INFORMATION:

You should carefully consider a Fund's investment objectives, risk factors, charges and expenses before investing. This and additional information can be found in the Fund's prospectus, which may be obtained by visiting: SDCI, USCI, ZSB, ZSC, USE, USG, BNO, CPER, UGA, UNG, UNL, USL, USO, UDI, UMI. Read the prospectus, and any applicable SAI, carefully before investing.

The information provided by USCF and its associated documents is intended to provide a broad overview for discussion purposes. It is subject to change and should not be taken as financial or investment advice. United States Commodity Funds LLC and USCF Investment Advisers, LLC make no offers to sell, solicitations to buy, or recommendations for any security, nor are they offering advisory services in connection with this information.

Past performance is not indicative of future results.

Statements herein may constitute forward-looking statements. You can identify these forward-looking statements by the use of words such as “outlook,” “believe,” “expect” or other comparable words. Forward-looking statements are subject to various risks and uncertainties. These forward-looking statements are based on USCF’s beliefs, assumptions and expectations, which can change as a result of many factors, not all of which are known to USCF or within its control. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements. No representation or warranty, express or implied, is made or given by or on behalf of USCF or any other person as to the accuracy and completeness or fairness of the information. Dated content speaks only as of the date indicated and we undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

Investing involves risk, including the possible loss of principal. It should not be assumed that any investment identified has been or will be profitable. There can be no guarantee that similar investment opportunities will be available in the future or that the strategy will be able to exploit similar investment opportunities should they arise.

Neither USCF nor ALPS Distributors, Inc. sponsor the opinions or information presented in posts, links or responses, nor do they assume liability for any loss that may result from relying on these opinions or information. Reposts, retweets and mentions do not represent endorsements.

Diversification does not eliminate the risk of experiencing investment losses.

Funds distributed by and not affiliated with ALPS Distributors, Inc.